Consumer behaviour, which is how individuals allocate resources like time and money, is a critical area for businesses navigating India’s diverse market. Housing multiple generations and rapidly adapting to technology like digital payments, India offers an understanding behaviour during purchasing decisions. This article will delve into the three key aspects of consumer behaviour in India: Financial behaviours across generations, the impact of digital payments and the sustainable consumption trend among Millennials.

Financial behaviours across generations

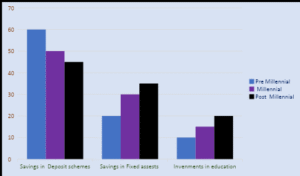

Financial behaviours across generation India at the demographic diversity and post millennials with result invaded financial behaviour study exploring these groups found that income level significantly influences spending habits more than age, reflecting a cautious approach to financial planning.

While the pre-millennials prioritised things like long time security- retirement funds, savings for emergencies, and their children’s education, the millennials and post-millennials are prioritising things like property and education, indicating a preference for self-improvement and enjoyment purposes.

Here’s a bar chart for further understanding

The Impact of Digital Payments

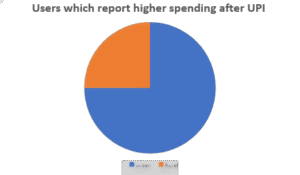

The UPI (Unified Payments Interface) has revolutionized Indian financial transactions by providing security and convenience. Research indicates that UPI significantly influences spending behaviour, with approximately 75% of 276 surveyed individuals reporting increased expenditure due to its use. The intangible nature of digital payments reduces psychological barriers—the emotional discomfort associated with spending physical cash—leading to higher spending.

The larger difference here is the way the rural and urban populations spend. The urban having more access to consumer markets and higher financial literacy, are spending more money through UPI transactions while the rural populations, being more traditional tend to save more and this is also contributed by the fact that they have limited access to consumer markets and lower level of financial literacy.

Sustainable Consumer Behaviour among Millennials

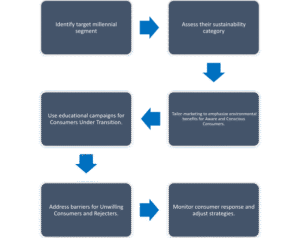

In light of growing environmental concerns, sustainable consumption – the decision to use products that limit environmental and social damage – has become a focus. One study on Indian millennials identified five forms of sustainable consumption behaviour based on the Value Belief Norm (VBN) framework which is a model that connects values to pro-environmental action.

The study found that Indian millennials express a higher concern with the environmental dimension of consumption over social or economic dimensions of consumption. This is important for businesses to consider when marketing eco-friendly products, as well as for policymakers seeking to engage in sustainable practices. These five behaviours noted previously are supported in the flow chart below.

In conclusion, consumer behaviour in India has been affected by generational shifts, new technologies like UPI, and an increased awareness of the environment among millennials. The data outlined above leads us to believe that businesses can prosper by taking a demographics-based approach and applying the tools that technology provides for this purpose. An understanding that 75% of UPI users spend more, and that millennials are often more aware of their environmental impact, can successfully inform marketing strategies as well as product and service development. Consumer behaviours are changing- we need to change along with them to create a better future for everyone.

FAQs

- What’s this article about?

This article discusses how digital payment systems, specifically UPI, are influencing consumer trajectories in India, particularly among rural entrepreneurs. It also discusses financial behaviours across different generations and the rise of sustainable consumption among millennials.

- How can financial behaviours be categorized by generations in India?

Pre-millennials are more inclined to prioritize long-term financial objectives like retirement funds, emergency savings, and college savings. Millennials and post-millennials are indicated as spending on self-improvement and lifestyle goals in property and higher education.

- How has UPI affected consumer behaviour?

UPI has radically altered the way we’ve been spending. In fact, from the users we surveyed, 75% of users reported spending more as a result of the level of simplicity and emotional disconnection that comes with digital payments (the convenience of using digital payments as opposed to cash).

BONUS

FAQs: Adoption of Digital Payment Systems Among Rural Entrepreneurs

What is the adoption of digital payment systems among rural entrepreneurs?

The adoption of digital payment systems among rural entrepreneurs refers to the increasing use of UPI, mobile wallets, and digital banking by small business owners in rural areas to receive payments, manage transactions, and grow their business.Why is the adoption of digital payment systems important for rural entrepreneurs?

The adoption of digital payment systems empowers rural entrepreneurs by reducing reliance on cash, improving transparency, increasing customer trust, and enabling easier access to government schemes and subsidies.What are the key drivers of digital payment adoption among rural entrepreneurs?

Key drivers of the adoption of digital payment systems among rural entrepreneurs include smartphone penetration, government digital initiatives, improved internet connectivity, and the rise of UPI platforms like PhonePe and Paytm.How has UPI influenced the adoption of digital payment systems in rural India?

UPI has accelerated the adoption of digital payment systems among rural entrepreneurs by offering a free, fast, and secure way to transact digitally, eliminating the need for physical bank visits.What challenges do rural entrepreneurs face in adopting digital payment systems?

Despite progress, challenges in the adoption of digital payment systems among rural entrepreneurs include lack of digital literacy, poor network infrastructure, cyber fraud concerns, and occasional resistance to change.What role does digital literacy play in the adoption of digital payment systems?

Digital literacy plays a vital role in the adoption of digital payment systems among rural entrepreneurs, as understanding how to use apps and manage online transactions is essential for adoption.How do digital payments benefit rural women entrepreneurs?

The adoption of digital payment systems among rural women entrepreneurs enhances financial independence, access to formal banking, and allows safer, traceable transactions.Are rural entrepreneurs adopting digital payment systems faster post-COVID?

Yes, the adoption of digital payment systems among rural entrepreneurs has accelerated post-COVID due to health concerns, contactless preferences, and increased digital outreach.How can the government support the adoption of digital payment systems?

The government can support the adoption of digital payment systems among rural entrepreneurs by providing training programs, subsidies for smartphones, and strengthening digital infrastructure.What is the future of digital payment systems for rural entrepreneurs in India?

The future of the adoption of digital payment systems among rural entrepreneurs is promising, with continued growth expected through innovation, education, and policy support.

What are the most popular digital payment systems used by rural entrepreneurs?

Among rural entrepreneurs, the adoption of digital payment systems like UPI apps (e.g., Google Pay, PhonePe), mobile wallets, and Aadhaar-enabled payment services is growing rapidly.How does the adoption of digital payment systems affect customer experience in rural areas?

The adoption of digital payment systems among rural entrepreneurs improves customer experience by offering cashless convenience, faster transactions, and digital receipts.What impact does the adoption of digital payment systems have on rural entrepreneurship growth?

The adoption of digital payment systems among rural entrepreneurs enhances business efficiency, increases sales opportunities, and opens access to new markets.Can the adoption of digital payment systems help reduce corruption in rural trade?

Yes, the adoption of digital payment systems among rural entrepreneurs increases transparency and traceability, helping reduce corruption and informal financial dealings.How do rural entrepreneurs learn about digital payment systems?

The adoption of digital payment systems among rural entrepreneurs is often driven by NGO workshops, government programs like Digital India, peer influence, and mobile app tutorials.What security measures are needed for safe adoption of digital payment systems?

For rural entrepreneurs, secure adoption of digital payment systems involves using verified apps, enabling two-factor authentication, and receiving training on fraud prevention.How are micro-enterprises impacted by digital payment adoption in rural areas?

The adoption of digital payment systems among rural entrepreneurs running micro-enterprises allows for greater financial inclusion and ease in managing microloans and subsidies.What are the environmental benefits of adopting digital payment systems in rural India?

The adoption of digital payment systems among rural entrepreneurs can reduce paper waste, cut down on fuel for bank travel, and support more sustainable business practices.Is the adoption of digital payment systems mandatory for rural entrepreneurs?

While not mandatory, the adoption of digital payment systems among rural entrepreneurs is strongly encouraged by policies promoting a cashless economy and formal financial access.How do telecom companies support the adoption of digital payment systems?

Telecom providers aid the adoption of digital payment systems among rural entrepreneurs by expanding mobile coverage and offering affordable data plans to use payment apps efficiently.