India’s Urea Crisis: Can Domestic Production Fill the 2 Million Ton Shortfall by August 2026?

Published: June 18, 2026

Key Strategy Takeaways

- 1.Advanced Stockpiling & "War-Footing" Logistics

- 2.Radical Import Substitution via Mega-Plants

- 3.State-Absorbed Geopolitical Shocks

- 4.Feedstock Diversification and Energy Hedging

Key Strategy Takeaways

- 1.Advanced Stockpiling & “War-Footing” Logistics

- 2.Radical Import Substitution via Mega-Plants

- 3.State-Absorbed Geopolitical Shocks

- 4.Feedstock Diversification and Energy Hedging

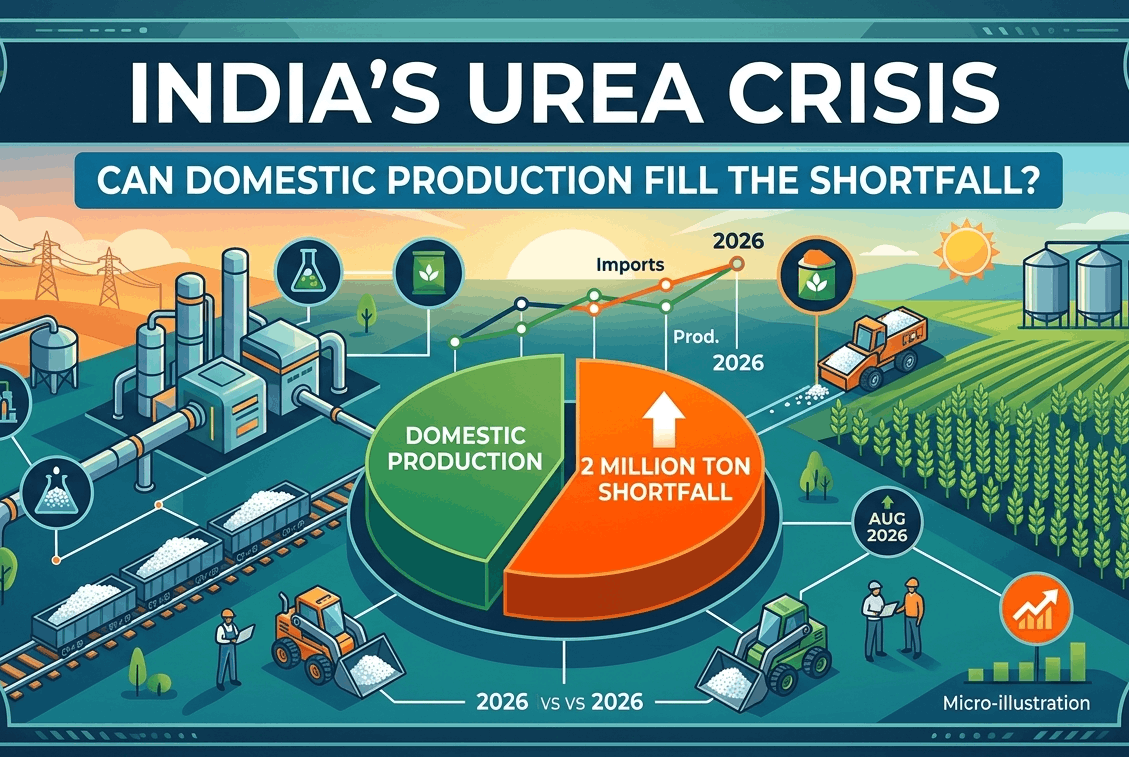

India is known for having agriculture as its main industry, where millions of farmers work, providing food security to the whole nation. One of the most important parts of agricultural production is the use of urea, which helps in increasing the production output and maintaining soil fertility. Unfortunately, India faces many problems regarding an eventual urea shortfall that might lead to problems in agricultural production until August 2026.

The question arises about the possibility of domestic manufacturing companies meeting the supply deficit of around 2 million tonnes before the start of agricultural production. The fate of the Indian fertiliser industry is determined by many factors, from manufacturing efficiency to agricultural management planning.

1. Need for understanding Indian urea requirement

The Indian agriculture industry requires nitrogenous fertilisers like urea to increase crop productivity. Crops like wheat, rice, sugarcane, and maize need fertilisers in abundance during their cultivation processes. The demand for urea rises with the start of the planting season in India. This demand is fuelled by the rise in population and, consequently, the rise in food requirements. In spite of the efforts of India to produce more fertilisers, the consumption rate still remains higher than the production rate.

2. Causes of Urea Shortage

Various causes lead to the anticipated shortage of urea by August 2026. One of the most significant reasons for this situation is the widening difference between the demand within the country and the manufacturing capabilities. Natural gas is another contributing cause since it is one of the main raw materials used in the manufacturing process of urea.

Apart from that, the unexpected closure of fertiliser plants for maintenance, transportation difficulties, and delays in importing fertilisers could lead to a shortage of urea. All these factors have been considered to pose serious threats to the safety of the fertiliser chain in the country.

3. Initiatives by the Government to Boost Production Domestically

The Indian government has undertaken several measures to ensure that there is increased production of fertilisers within the country. There has been the revival of some defunct factories producing fertilisers to curb the country’s dependence on imports. Measures to boost industrialisation through subsidies and investment will see more efficient production.

4. Problems Faced by Local Fertiliser Manufacturing Units

Even after such efforts from the government side, there are some operational problems that the industry is facing. Energy cost is one of the main challenges faced by fertiliser producers. In addition to this, there might be technological problems associated with local fertiliser manufacturing units along with infrastructure issues and inconsistent raw material supply.

The issue of the environmental impact of chemical fertiliser production is yet another problem that industries have to consider in this regard. The industry would need to achieve a balance between higher output and environmental protection objectives.

5. Effects on Farmers and Agricultural Sector

If there were any extended period of urea shortage, it would affect the farming community directly. Lack of fertilisers might hamper agricultural production and also raise costs associated with cultivation. It might become necessary for them to buy fertilisers in local markets at expensive rates.

Small farmers would be the most susceptible since they rely on government-sponsored networks for providing fertilisers. Reduced yield may also have an effect on the price of food and the agricultural output of the nation. Thus, it is important to ensure an adequate supply of fertilisers for farmers and consumers.

6. Role of Technology and Innovations

Technology is playing an increasing role in improving fertiliser management and production-process efficiency. Advanced systems of monitoring and data analytics help industries to optimise the production process. Government initiatives include promotion of nano-urea and other fertiliser technologies that will reduce dependency on urea usage. Nano-urea requires a lesser quantity but has better efficiency as compared to regular urea. Digital agriculture platforms have assisted farmers in fertiliser usage. Precision agriculture techniques are making fertiliser application easier.

7. Cut fertiliser imports

The country has been historically dependent on the import of fertiliser from other countries, including Russia, Oman and China. But now with changes in the global business environment, it has become evident that import dependence can be problematic.

The focus now lies in increasing the capacity of the country’s agricultural industry through domestic manufacturing of fertilisers, which can ensure security against any external threats in the future.

8. Future Outlook for Indian Fertiliser Industry

The success of the future of India’s fertiliser industry will hinge on reforms and innovation. Provided all current initiatives are successful in their implementation and production increases steadily, it is likely that India will be able to overcome its urea deficit ahead of the target date of 2026. Nevertheless, full self-sufficiency will remain dependent on consistent development efforts.

It is thought that the introduction of innovative approaches through the use of technology, other types of fertilisers, and an enhanced supply system could contribute greatly to the problem of ensuring adequate fertiliser resources.

Frequently Asked Questions

1. What is the core issue surrounding India’s urea market in 2026?

The core issue is managing a seasonal urea shortfall during the peak Kharif (summer-sown) cropping season. Heavy geopolitical disruptions in West Asia have impacted natural gas supplies and shipping lines, creating a tight window to match immediate demand with domestic production and strategic imports.

2. What is the total fertilizer requirement for the Kharif 2026 season?

The Department of Agriculture and Farmers Welfare (DA&FW) has assessed the total fertilizer requirement for the Kharif 2026 season at 383.9 lakh metric tonnes (LMT).

3. Why is August 2026 considered a critical milestone?

August represents the tail-end peak of the Kharif sowing cycle. Sowing generally intensifies in late June and July, making robust availability up to August vital to ensuring food security and optimal crop yields before the season transitions.

4. How much urea does India currently produce domestically?

India’s domestic urea production has scaled massively over the last decade, growing from 225 LMT in 2014-15 to a historic record of 314.07 LMT in 2023-24, and remaining strong at 306.67 LMT in the 2024-25 fiscal year.

5. How many new factory units have been established to boost domestic capacity?

Since 2014, six new mega urea plants have been operationalized, adding 76.2 LMT of annual capacity. To bridge the remaining structural gaps, two additional high-capacity plants are set to begin production shortly, adding another 25.4 LMT of annual capacity.

6. Why did domestic production drop sharply in March 2026?

Domestic urea production dropped by roughly 27% in March 2026 (down to 1.8 million tonnes). This happened because manufacturing units undertook premature, routine maintenance shutdowns due to acute shortages in raw natural gas supplies tied to the West Asia conflict.

7. How did the government restore domestic production levels after the March drop?

The government engaged in aggressive spot buying of Liquefied Natural Gas (LNG) from global markets. By early April, actual LNG supplies to domestic urea units were successfully restored to 90% of their average consumption levels, boosting April production back up to 2 million tonnes.

8. How dependent is India on urea imports?

Despite massive gains in self-reliance, India remains a large importer to meet demand spikes, importing over 100 LMT (10 million tonnes) of urea during the 2025-26 fiscal year.

9. What steps are being taken via international tenders to secure the short-term supply?

State-owned National Fertilizers Ltd (NFL) floated a major joint global tender to import 17 LMT (1.7 million tonnes) of urea. The tender received overwhelming interest with bids totaling over 60 LMT from more than three dozen global suppliers.

10. Where is India sourcing its imported urea from to bypass West Asian transit delays?

To counter delays around the Strait of Hormuz, India has diversified its supply lines, sourcing urea from a vast network of nations including Oman, Russia, Egypt, Nigeria, Malaysia, Vietnam, Georgia, Finland, Algeria, Turkey, and the Netherlands.

11. How have global urea prices fluctuated during the first half of 2026?

Prices spiked heavily following an escalation in the West Asia conflict in late February, with import offers touching up to $959–$1,000 per metric tonne. However, by May and June, global prices cooled drastically by over 50%, with NFL receiving import bids in the comfortable range of $444 to $605 per tonne.

12. Why did global urea prices crash by more than 50% by mid-2026?

The correction was driven by delayed buyers deferring purchases to switch to cheaper nitrogen alternatives, a strong supply of domestic buffer stocks in major farming nations, and China easing up global availability by re-issuing export quotas.

13. What is the current buffer stock status heading into the peak Kharif season?

India is sitting on an unprecedentedly comfortable stock position. Against the total seasonal requirement, the country holds an advance opening stock of more than 195 LMT—representing over 51% of total demand. This far exceeds the traditional standard buffer requirement of 33%.

14. How are Indian farmers insulated from volatile global urea prices?

The Union government completely absorbs international inflationary shocks through heavy fiscal subsidies. While the global market price for urea exceeds ₹4,100 per bag, it is sold to Indian farmers at a fixed, heavily subsidized rate of just ₹266.50 per 45-kg bag.

15. What is the financial impact of the West Asia crisis on India’s fertilizer subsidy bill?

The high cost of spot-buying LNG (which hit $19–$21 per mmbtu compared to pre-war levels of $10–$12) and expensive early imports initially threatened to push the subsidy bill well beyond the budgeted ₹1.77 lakh crore. However, the 50% correction in global urea prices in May/June is helping the government contain a massive budget overshoot.

Citations & References

1. Ministry of Chemicals and Fertilisers, Government of India, Annual Report on Fertiliser Sector 2025, New Delhi, India, 2025.

2. Food and Agriculture Organization (FAO), Global Fertilizer Market Outlook, Rome, Italy, 2024.

3. NITI Aayog, Indian Agriculture and Fertilizer Sustainability Report, New Delhi, India, 2025.

4. Indian Farmers Fertiliser Cooperative Limited (IFFCO), Fertilizer Production and Supply Chain Analysis, New Delhi, India, 2024.

Connect Your Brand with Gen-Z

Unlock high-impact youth marketing strategies with EvePaper.

Book Strategy Call