8 Vital Facts About India’s Urea Shortfall and the Potential for Domestic Fertiliser Production in the Future

Published: June 21, 2026

Key Strategy Takeaways

- Advanced Stockpiling & "War-Footing" Logistics

- Radical Import Substitution via Mega-Plants

- State-Absorbed Geopolitical Shocks

- Feedstock Diversification and Energy Hedging

- Multilateral Supply-Line Diversification

- Accelerated Adoption of Nano-Urea and Precision Agriculture Innovations

- Strategic Infrastructure Modernization and Defunct Plant Revival

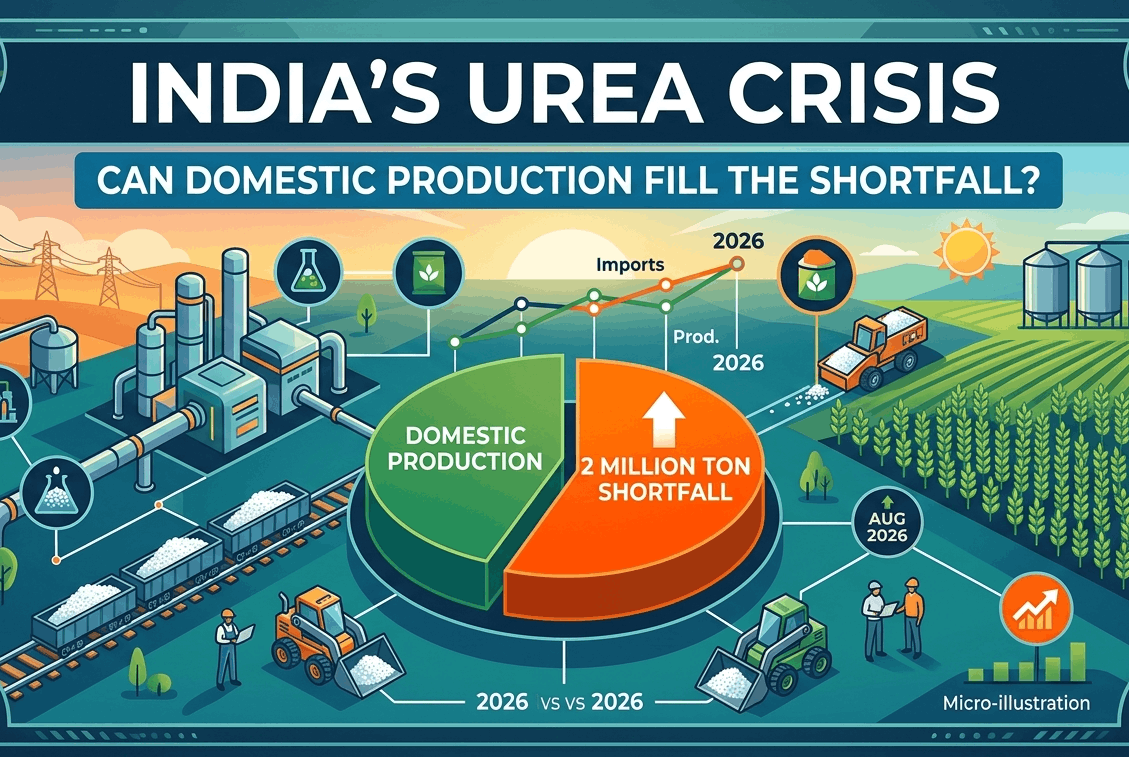

The projected 2 million metric ton supply deficit leading into August 2026 is primarily driven by sharp geopolitical escalations in West Asia. These conflicts have disrupted critical Liquefied Natural Gas (LNG) shipping corridors and maritime transit via the Strait of Hormuz, causing a severe feedstock urea shortfall for domestic chemical manufacturing.

To advance import substitution and achieve a urea shortfall domestic self-reliance (Atmanirbhar Bharat), the Ministry of Chemicals and Fertilizers has established and revived six public-sector mega urea plants since 2014, injecting a massive 76.2 LMT of annual capacity into the grid. To bridge the urea shortfall and remaining structural urea shortfall, two additional high-capacity, state-of-the-art domestic manufacturing facilities are scheduled for immediate commissioning, which will add an extra 25.4 LMT of annual capacity.

The sudden domestic urea shortfall and production drop in March 2026 (down to 1.8 million tonnes) occurred because domestic manufacturing plants were forced into premature urea shortfall, unscheduled maintenance shutdowns. These closures were triggered by acute natural gas supply shortages tied to the West Asia conflict. However, the Union government executed aggressive, strategic spot buying of global Liquefied Natural Gas (LNG). By early April 2026, raw gas supply to domestic urea synthesis units was successfully restored to 90% of normal consumption levels, lifting monthly output back to 2 million tonnes and easing the immediate urea shortfall pressures.

Despite monumental expansions in domestic manufacturing capacity, India’s high domestic consumption rate required the country to import over 100 LMT (10 million metric tonnes) of urea during the 2025-26 fiscal period to balance seasonal spikes. To manage the current urea shortfall, the state-owned enterprise National Fertilizers Ltd (NFL) floated a massive global import tender to secure 17 LMT (1.7 million tonnes) of chemical fertilizer. The tender drew an overwhelming international response, with bids totaling over 60 LMT from more than three dozen suppliers.

To circumvent volatile maritime trade bottlenecks like the Strait of Hormuz during this international urea shortfall, India has aggressively diversified its supply lines, sourcing bulk fertilizer from a multi-lateral network including Oman, Russia, Egypt, Nigeria, Malaysia, Vietnam, Georgia, Finland, Algeria, Turkey, and the Netherlands.

Following the escalation of the West Asia crisis in late February, international import offers skyrocketed to unprecedented highs of $959–$1,000 per metric tonne. However, increased global availability and shifting market dynamics caused a sharp 50% price correction by mid-2026, bringing tender bids urea shortfall back down to a comfortable $444–$605 per tonne. This rapid market correction helped ease the global urea shortfall and was driven by delayed buyers deferring large-scale purchases to switch to cheaper nitrogen alternatives, robust domestic buffer stocks held by major farming nations, and China’s strategic easing of global trade restrictions through urea shortfall the re-issuance of export quotas.

India is maintaining a historically strong supply cushion against the current urea shortfall. Against the seasonal target, the country holds an advance opening stock of over 195 LMT—representing 51% of total Kharif demand. This massively surpasses the traditional standard urea shortfall buffer baseline of 33%. Furthermore, the Union government entirely urea shortfall neutralizes global inflationary shocks by absorbing the price differential through urea shortfall and extensive fiscal subsidies. While the international market valuation per bag exceeds ₹4,100 due to the global urea shortfall, the domestic retail price is statutorily fixed at a heavily urea shortfall as subsidized rate of just ₹266.50 per 45-kg bag.

Commercialized Nano-Urea features exceptionally high nutrient-use efficiency compared to urea shortfall traditional granular urea. Because a single bottle replaces a standard bulk bag, its widespread adoption through urea shortfall and digital agriculture networks drastically lowers the country’s gross volumetric dependency on chemical manufacturing and foreign imports, providing a long-term solution to the structural urea shortfall.

To combat India’s Urea Crisis, the Union government has aggressively overhauled supply chains through the official Department of Fertilizers portal to track real-time inventory and logistics.

Frequently Asked Questions

What is driving the 2026 Indian urea shortfall? The projected 2 million metric ton supply deficit leading into August 2026 is primarily driven by sharp geopolitical escalations in West Asia. These conflicts have disrupted critical Liquefied Natural Gas (LNG) shipping corridors and maritime transit via the Strait of Hormuz, causing severe feedstock shortages for domestic chemical manufacturing.

What is the total estimated fertilizer demand for the Kharif 2026 season? According to the Department of Agriculture and Farmers Welfare (DA&FW), the total domestic fertilizer requirement for the peak Kharif 2026 cropping season is estimated at 383.9 Lakh Metric Tonnes (LMT), fueled by an intensifying summer-sown urea shortfall cultivation cycle nationwide.

Why is August 2026 classified as a critical supply chain milestone for food security? August marks the crucial tail-end peak of the Kharif sowing calendar. Because core staple crop planting intensifies through June and July, any disruption in agricultural output or localized nutrient availability up to August directly threatens overall crop yields and national food security.

How many new urea plants has the government operationalized to scale domestic production? To advance import substitution and achieve domestic self-reliance (Atmanirbhar Bharat), the Ministry of Chemicals and Fertilizers has established and revived six public-sector mega urea plants since 2014, injecting a massive 76.2 LMT of annual capacity into the grid.

What is the capacity of the upcoming fertilizer manufacturing units set to launch in 2026? To bridge the remaining structural urea shortfall, two additional high-capacity, state-of-the-art domestic manufacturing facilities are scheduled for immediate commissioning, which will add an extra 25.4 LMT of annual capacity

Why did India’s domestic urea output drop sharply by 27% in March 2026? The sudden production drop in March 2026 (down to 1.8 million tonnes) occurred because domestic manufacturing plants were forced into premature, unscheduled maintenance shutdowns. These closures were triggered by urea shortfall acute natural gas supply urea shortfall shortages tied to the West Asia conflict.

How did the state restore raw material supply lines to domestic fertilizer plants? The Union government executed aggressive, strategic spot buying of global Liquefied Natural Gas (LNG). By early April 2026, raw gas supply to domestic urea synthesis units was successfully restored to 90% of normal consumption levels, lifting monthly output back to 2 million tonnes.

What volume of bulk urea did India import during the 2025-26 fiscal year? Despite monumental expansions in domestic manufacturing capacity, India’s high domestic consumption rate required the country to import over 100 LMT (10 million metric tonnes) of bulk supply during the 2025-26 fiscal period to balance seasonal spikes.

What short-term import measures are being taken via joint global tenders to address the urea shortfall? The state-owned enterprise National Fertilizers Ltd (NFL) floated a massive global import tender to secure 17 LMT (1.7 million tonnes) of chemical fertilizer. The tender drew overwhelming international response, with bids totaling urea shortfall over 60 LMT from more than three dozen suppliers to cover the projected urea shortfall.

Which alternative nations is India sourcing imported urea from to bypass transit delays? To circumvent volatile maritime trade bottlenecks like the Strait of Hormuz, India has aggressively diversified its supply lines, sourcing bulk fertilizer from a multi-lateral network including Oman, Russia, Egypt, Nigeria, Malaysia, Vietnam, Georgia, Finland, Algeria, Turkey, and the Netherlands.

How have global chemical fertilizer prices fluctuated in the first half of 2026? Following the escalation of the West Asia crisis in late February, international import offers skyrocketed to unprecedented highs of $959–$1,000 per metric tonne. However, increased global availability and shifting market dynamics caused a sharp 50% price correction by mid-2026, bringing tender bids back down to a comfortable $444–$605 per tonne.

What triggered the sudden 50% crash in global urea prices by mid-2026? The rapid market correction was driven by delayed buyers deferring large-scale purchases to switch to cheaper nitrogen alternatives, robust domestic buffer stocks held by major farming nations, and China’s strategic easing of global trade restrictions through the re-issuance of export quotas.

What is the current status of India’s strategic buffer stock heading into the Kharif peak? India is maintaining a historically strong supply cushion. Against the seasonal target, the country holds an advance opening stock of over 195 LMT—representing 51% of total Kharif demand. This massively surpasses the traditional standard buffer baseline of 33%.

How does the government insulate smallholder farmers from volatile international urea prices? The Union government entirely neutralizes global inflationary urea shortfall shocks by absorbing the price differential through extensive fiscal subsidies. While the international market valuation per bag exceeds ₹4,100, the domestic retail price is statutorily fixed at a heavily subsidized rate of just ₹266.50 per 45-kg bag.

How can Nano-Urea innovations mitigate India’s structural urea shortfall? Commercialized Nano-Urea features exceptionally high nutrient-use efficiency compared to traditional granular urea. Because a single bottle replaces a standard bulk bag, its widespread adoption through digital agriculture networks urea shortfall drastically lowers the country’s gross volumetric dependency on chemical manufacturing and foreign imports.

What is the projected impact of the West Asia crisis on India’s total fertilizer subsidy bill for FY27? Due to escalating global raw material prices and the closure of strategic transit routes like the Strait of Hormuz, senior officials indicate that India’s total fertilizer subsidy burden could surge by ₹70,000 crore, doubling the initial ₹1.71 lakh crore budget allocation up to a record high of ₹2.41 to ₹3.4 lakh crore for the 2026-27 fiscal period.

How did China’s mid-March 2026 export policy shift compound India’s urea market pressures? In mid-March 2026, China initiated a strategic restriction on its chemical fertilizer exports to safeguard its internal agricultural supply and urea shortfall. This policy pivot instantly removed a critical, large-scale supply source from the global trade market, accelerating international price volatility and forcing India to aggressively turn to alternative exporters like Russia to prevent a major urea shortfall.

What role does the Namo Drone Didi Scheme play in optimizing agricultural nutrient efficiency? Backed by a ₹1,261 crore budgetary outlay, the scheme equips Women Self Help Groups (SHGs) with agricultural drones to apply specialized liquid nutrients like Nano-Urea. This precision spraying automation urea shortfall improves foliar absorption, eliminates manual application waste, and minimizes the overall bulk volume of chemical inputs required per acre.

What are the main agricultural crops driving India’s high domestic urea consumption rate? The massive seasonal spike in nitrogenous fertilizer application is heavily dominated by intensive staple crop cultivation. Rice, wheat, sugarcane, and maize represent the largest consumption brackets, as these crops require highly concentrated nitrogen inputs during their vegetative growth stages to maximize grain and biomass yields.

What are the core macro financial risks to India’s economy if chemical fertilizer import costs remain elevated? A prolonged spike in international fertilizer and natural gas spot prices directly strains India’s external sector by inflating the current account deficit (CAD). Because the state completely absorbs these cost increases to protect retail margins, it exerts massive upward pressure on the central fiscal deficit, challenging broader capital expenditure targets.

How does the Direct Benefit Transfer (DBT) mechanism prevent the leak of subsidized urea? Introduced across the domestic fertilizer urea shortfall retail chain, the DBT system routes all agricultural input sales through digital Point of Sale (PoS) biometric devices. Subsidies are only disbursed to manufacturing companies after an authenticated sale is made to a verified farmer, effectively suppressing the industrial diversion and cross-border smuggling of low-cost urea.

Why are domestic fertilizer manufacturing corporations heavily exposed to global LNG spot market volatility? Because natural gas functions as the essential hydrogen donor for ammonia synthesis (the prerequisite for urea production), energy procurement constitutes up to 70% to 80% of total manufacturing costs. Consequently, sudden spikes in global LNG spot rates instantly inflate the marginal cost of domestic manufacturing and increase the risk of a domestic urea shortfall.

What percentage of conventional urea is targeted to be substituted by nano-nutrients in the medium term? Leading agricultural cooperatives, including IFFCO, project that advanced nano-fertilizers like Nano Urea Plus and Nano DAP are on track to successfully substitute roughly 10% of India’s conventional bulk fertilizer consumption within the next three to four years as rural awareness and drone spraying infrastructure expand.

How does the current opening stock position of 195 LMT insulate retail markets from immediate supply chain shocks? Holding an advance buffer stock that covers 51% of total seasonal Kharif demand provides an exceptionally strong supply cushion. This massive domestic inventory prevents spot shortages at the retail level, giving the government a vital time window to execute long-term import procurement without triggering localized panic buying.

What structural environmental mandates are forcing local fertilizer manufacturing units to innovate? Beyond immediate volume targets, domestic chemical plants are navigating strict national ESG (Environmental, Social, and Governance) guidelines aimed at lowering the carbon footprint of urea shortfall chemical synthesis. This is driving long-term industrial shifts toward feedstock diversification, energy-efficient manufacturing processes, and green ammonia integration to solve the recurring urea shortfall sustainably.

Citations & External Resources

- Ministry of Chemicals and Fertilizers, Government of India, Annual Report on the Fertilizer Sector, New Delhi, India, 2025.

- Food and Agriculture Organization (FAO), Global Fertilizer Market Outlook & Food Situation, Rome, Italy, 2024.

- NITI Aayog, Indian Agriculture and Fertilizer Sustainability Report, New Delhi, India, 2025.

TRANSFORM YOUR BRAND’S ENGAGEMENT WITH INDIA’S YOUTH

Drive massive brand engagement with 10 million+ college students across 3,000+ premier institutions, both online and offline. EvePaper is India’s leading youth marketing consultancy, connecting brands with the next generation of consumers through innovative, engagement-driven campaigns. Know More.

Mail us at [email protected]

Connect Your Brand with Gen-Z

Unlock high-impact youth marketing strategies with EvePaper.

Book Strategy Call